You have some money left after expenses, and now you are stuck. Should you keep it safe in the bank, or put it into mutual funds and stocks so it grows?

Ask ten people and you will get ten answers. Some say always invest, money in the bank is wasted. Others say save first, the market is too risky. Both are partly right and partly wrong.

The truth is simpler. You shouldn’t treat saving and investing as opposing options, but rather as two complementary tools that work together. They are two stages, and doing them in the right order is what keeps you safe and growing at the same time.

“Saving keeps you standing. Investing helps you climb. You need to stand before you climb.”

Let us clear up what each one actually does, and then settle the order once and for all.

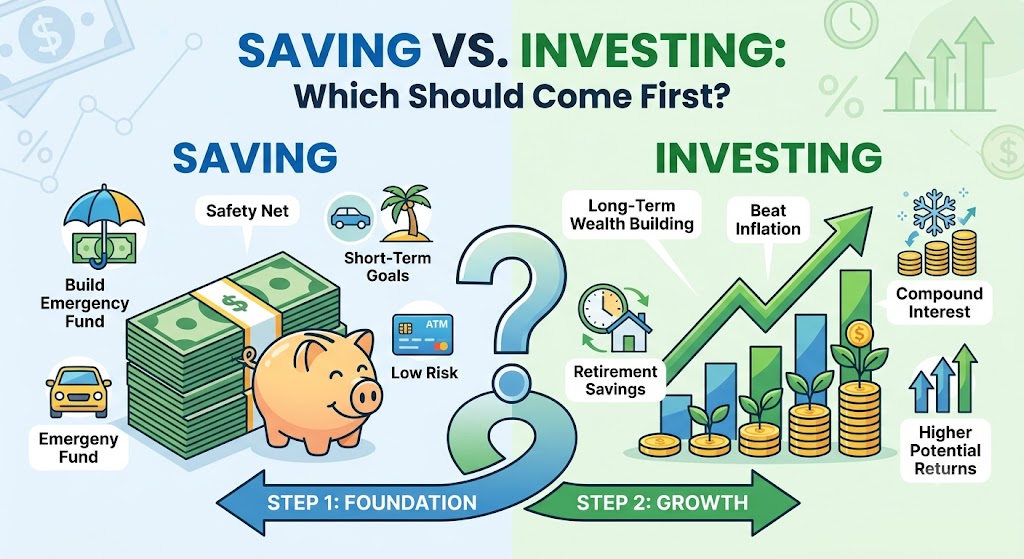

What Saving Really Means

Saving is keeping money safe and within reach. It goes into a bank account, a fixed deposit, or a liquid fund. It does not grow much, and that is fine, because growth is not its job.

The job of savings is to be there when you need it. It helps improve your peace when you’re in need of money.

“Savings are not meant to grow. They are meant to be ready.”

You save for things like:

- Emergencies — a job loss, a medical bill, or an urgent repair.

- Short-term goals — money you will need within one to three years.

- Peace of mind — a cushion so one bad month does not become a crisis.

What Investing Really Means

Investing is putting money to work so it grows over time. It goes into assets like stocks, mutual funds, or property, which can rise in value or pay you returns.

The trade-off is risk. Investment returns can fall in short term, and they may not be easy to pull out at a moment you need. In return, they beat inflation and build real wealth over years.

“Saving protects your money from emergencies. Investing protects it from inflation.”

You invest for things like:

- Long-term wealth — retirement, a house, or a child’s education years away.

- Beating inflation — so your money does not quietly lose value sitting idle.

- Compounding — letting returns earn their own returns, given enough time.

So Which Comes First? Saving.

Here is the answer, plain and simple: saving comes first. Before you invest a single rupee, you need a safety net in place.

The reason is risk. If you invest everything and an emergency hits, you may be forced to sell your investments at a bad time, often at a loss. A small savings buffer stops that from ever happening.

“Never invest money you might need tomorrow. That is what savings are for.”

Build your base in this order:

- Starter savings — a small buffer of one month’s expenses to handle small shocks.

- Emergency fund — three to six months of expenses kept safe and liquid.

- Then invest — once the cushion is set, send your extra money into investments.

The One Exception: Don’t Wait Too Long

Saving first does not mean saving forever before you touch investing. If you spend years only building savings, you lose the most powerful thing investing offers: time.

So the smart move is to build a basic safety net quickly, then start investing even while you finish topping up the savings fund. The two can overlap once you have a small cushion.

“Start the safety net first, but do not let it delay your first investment for years.”

A simple way to balance both:

- Phase 1 — focus most of your saving on a starter fund of one month’s expenses.

- Phase 2 — split your money: keep building the emergency fund and begin small investments.

- Phase 3 — with the full fund done, direct the bulk of your surplus into investing.

A Simple Order to Follow

If you want one clear path instead of theory, here it is. Walk down this list and only move to the next step once the current one is handled.

It works whether you earn a little or a lot. The amounts change, the order does not.

“Money is simple when you follow the order. It gets messy when you skip steps.”

The order of priority:

- Clear high-interest debt — credit card dues, personal loan or any other costly loans come before anything else.

- Build a starter fund — one month of expenses, kept safe and easy to reach.

- Complete the emergency fund — grow it to three to six months of expenses.

- Invest for the long term — once safe, put surplus money to work and let it compound.

The Takeaway

Saving and investing are not enemies, and you do not have to choose one for life. You save first to stay safe, then you invest to grow. The order matters more than the labels.

Here is the whole idea in one glance:

- Saving keeps money safe and ready for emergencies

- Investing grows money over the long term and beats inflation

- Save first — build a safety net before you invest a rupee

- Do not wait too long — start investing once a basic cushion is in place

- Follow the order — clear bad debt, save, then invest

“First make your money safe. Then make it grow. In that order, both win.”

Look at your money today and find your step on the list. Whatever stage you are at, the next move is already clear.

Where are you right now — saving, investing, or both? Tell us in the comments, and share this with someone stuck on the same question.

Leave a Reply