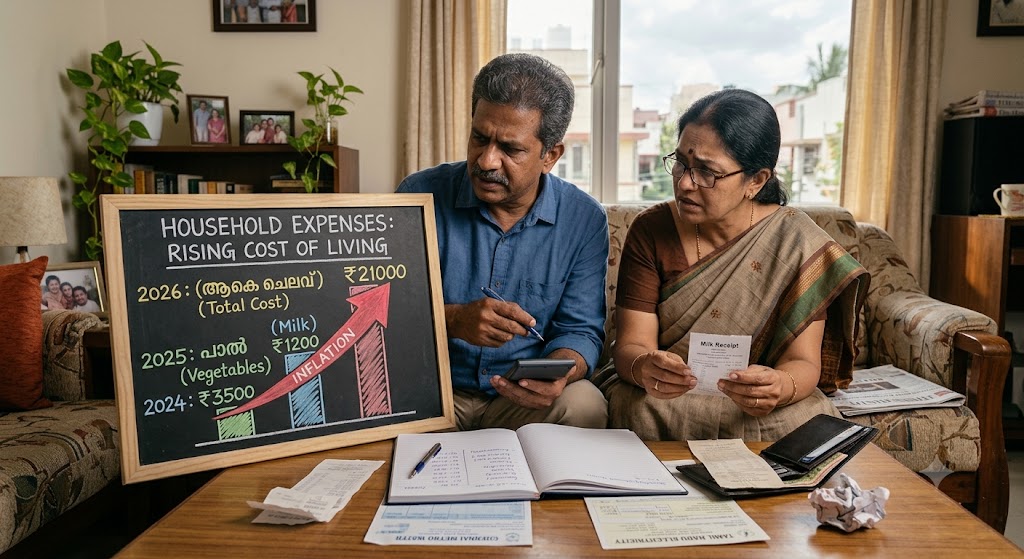

Think back to what ₹100 could buy you ten years ago, and what it buys today. The same note is now worth far less. Your money did not change, but some force pulled it to less. That invisible force is inflation.

Inflation is one of the most important factors in personal finance, and one of the most ignored. It works silently in the background, year after year, slowly draining the value of every rupee you own.

The frustrating part is that you can be do everything such as earning, saving, being careful, and still get poorer over time if you ignore inflation. Understanding inflation is the first step to protecting yourself from it.

“Inflation is the tax nobody can ignore and everybody pays.”

Let us break down what inflation is, how it affects your money, and how to fight back.

What Inflation Actually Is

Inflation simply means the general rise in prices over time. As prices go up, each rupee is worth a little less than before. Your money slowly loses its purchasing power, even while sitting as cash.

It is not usually dramatic. A few percent a year sounds small and harmless. But over many years, that small, steady rise adds up to a huge loss in what your money can actually do.

“Inflation does not steal your money. It steals what your money can buy.”

The core idea:

- Prices rise — the same goods cost more over time.

- Money weakens — each rupee is worth less than it used to.

- It is constant — a slow, steady erosion, year after year.

The Silent Damage to Savings

Here is the hard truth many people miss: money sitting idle in a savings account or at home is silently losing value every year. If inflation is higher than the interest you earn, you will lose your money over time.

This is why “just keeping it safe” is not always safe. Cash feels secure, but inflation eats it in the background. The money looks the same, yet it is worth less each year.

“Cash under the mattress does not stay still. It shrinks in silence.”

How inflation hurts idle money:

- Low-interest accounts — often earn less than inflation, so you lose real value.

- Cash at home — loses buying power every single year.

- The illusion of safety — the number stays the same, but its worth falls.

Why Real Returns Matter More

Because of inflation, the return you see is not the return you get. A 6% interest rate with 6% inflation is a real return of zero. This gap is what really decides whether your money grows.

The number that matters is your real return, what is left after subtracting inflation. Always judge your investments by this, not by the headline rate that looks good on paper.

“It is not what your money earns that counts. It is what it earns after inflation.”

Understanding real returns:

- Nominal return — the headline rate you see advertised.

- Real return — that rate minus inflation, the true growth.

- The gap — a high rate can still mean zero real growth.

How Inflation Affects Your Daily Life

Inflation is not just an abstract number in the news. It shows up in your groceries, your fuel, your rent, and your bills. When your income does not grow with rising inflation, your lifestyle quietly shrinks.

This is why a raise that just matches inflation is not really a raise; it only keeps you in place. To truly grow ahead, your income and investments must grow faster than prices.

“If your income grows slower than prices, you are getting poorer while earning more.”

Where you feel it:

- Rising bills — groceries, fuel, and rent cost more each year.

- Flat raises — a small hike may not even cover higher prices.

- Shrinking lifestyle — the same income buys a little less over time.

How to Protect Your Money From Inflation

The good news is that you are not helpless. While you cannot stop inflation, you can protect your money by putting it into things that grow faster than the rate of inflation rise.

The key is to not let large amounts sit idle in low-return investments. Instead, invest in assets that historically beat inflation over the long run, so your wealth grows in real terms, not just on paper.

“You cannot avoid inflation. But you can outrun it.”

Ways to beat inflation:

- Invest in equity — stocks and equity funds have historically beaten inflation over the long term.

- Own some gold — often holds value when money loses it.

- Avoid idle cash — keep only what you need liquid; invest the rest.

Keep Only What You Need in Cash

This does not mean cash is useless. You still need an emergency fund and money for short-term needs, kept safe and accessible. The mistake is holding more cash than necessary.

Keep enough for emergencies and near-term goals, then put the rest to work in growth assets. This way you stay both safe and protected from inflation’s slow bite.

“Keep enough cash to sleep well, and invest the rest to grow well.”

A sensible balance:

- Emergency fund — a few months of expenses, kept safe and liquid.

- Short-term money — needs within a year or two, kept accessible.

- Everything else — invested to grow ahead of inflation.

The Takeaway

Inflation is the silent force that decides whether your hard-earned money grows or shrinks over the years. Ignore it, and you slowly get poorer. Understand it, and you can build wealth that truly lasts.

Here is the whole idea in one glance:

- What it is — prices rise, so money is worth less over time

- The silent damage — idle cash loses value every year

- Real returns matter — judge growth after subtracting inflation

- It hits daily life — bills rise, flat raises fall behind

- Beat it by investing — put money in assets that outgrow prices

- Hold only needed cash — safe money for now, growth for the rest

“The goal is not just to save money, but to make sure your money does not quietly lose its worth.”

Look at where your money sits today and ask one question: is it growing faster than prices, or slowly shrinking? The answer will tell you your next move.

How do you protect your money from inflation? Share your strategy in the comments, and pass this on to someone letting their savings sit idle.

Leave a Reply