The word “budget” makes most people feel awkward. It sounds like spreadsheets, restrictions, and tracking every rupee until the joy of life drains away. So most of us never make one, and our money slips through our fingers unplanned.

But budgeting does not have to be complicated or painful. In fact, one of the most popular budgeting methods in the world is so simple you can remember it in seconds. It is called the 50/30/20 rule.

This single, easy framework tells you exactly how to divide your income so you cover your needs, enjoy your life, and still build wealth, all without tracking every little expense. Here is how the 50/30/20 rule works and how to use it.

“A good budget does not restrict your life. It gives your money a clear job.”

Let us break down this simple budgeting rule step by step.

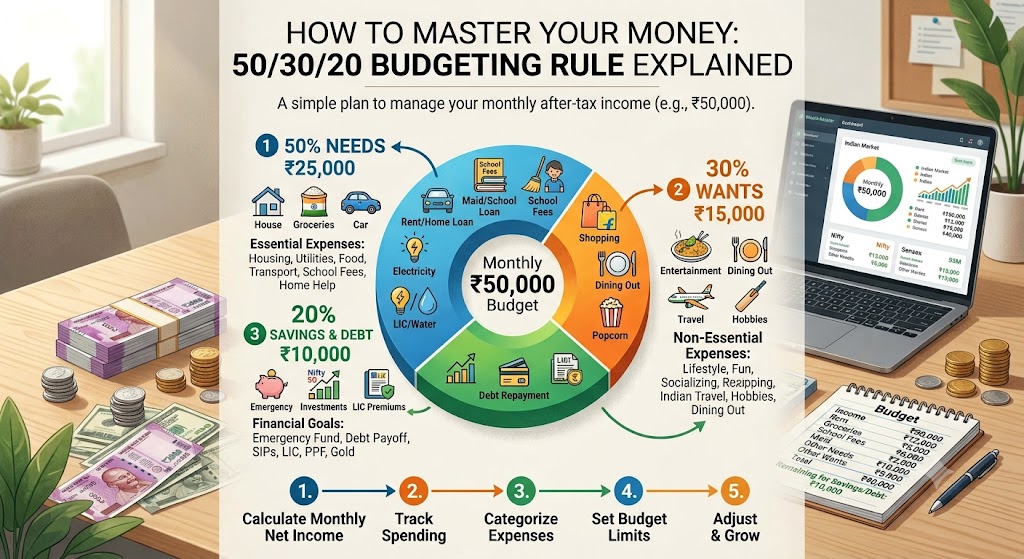

What the 50/30/20 Rule Is

The rule is beautifully simple. You divide your after-tax income into three broad buckets: 50% for needs, 30% for wants, and 20% for savings and debt repayment. That is the entire system.

Instead of tracking dozens of categories, you only manage three. This simplicity is its genius; it is easy to understand, easy to follow, and flexible enough for almost anyone to use.

“Three buckets, one simple rule. That is all budgeting needs to be.”

The three buckets:

- 50% Needs — essentials you cannot live without.

- 30% Wants — the things that make life enjoyable.

- 20% Savings — building wealth and clearing debt.

The 50%: Your Needs

The largest bucket covers your needs, the essential expenses you must pay to live and work. These are non-negotiable costs that keep your life running. The rule suggests keeping these to around half your income.

If your needs take up far more than 50%, it is a signal to look at your highest costs, like housing, and see if they can be reduced. Keeping needs in check leaves room for the other two buckets.

“Needs are what you cannot skip. Keep them lean to free up the rest.”

What counts as needs:

- Housing — rent or home loan EMI.

- Essentials — groceries, utilities, and transport.

- Obligations — insurance, minimum loan payments, and basic bills.

The 30%: Your Wants

This bucket is what makes the rule livable. Wants are the non-essential things that make life enjoyable, and the rule deliberately allows for them. You are not meant to live like a monk.

Eating out, entertainment, hobbies, travel, and upgrades all fall here. Giving yourself a clear, guilt-free allowance for wants is exactly why this budget is sustainable; it does not demand misery.

“A budget that bans all fun is a budget you will abandon. Wants are allowed.”

What counts as wants:

- Entertainment — dining out, movies, and subscriptions.

- Lifestyle — hobbies, travel, and shopping for pleasure.

- Upgrades — nicer versions of things you could get cheaper.

The 20%: Savings and Debt

This is the bucket that builds your future. At least 20% of your income goes toward savings, investments, and paying down debt beyond the minimums. This is where wealth is silently created.

Treat this bucket as a priority, not an afterthought. Ideally, you fund it first, before spending on wants, so your future is secured before your present pleasures. This is where the magic happens.

“The 20% bucket is small in size but mighty in building your future.”

What goes in this bucket:

- Savings — your emergency fund and short-term goals.

- Investments — for long-term wealth and retirement.

- Extra debt payments — clearing loans faster than the minimum.

How to Actually Apply It

Putting the rule into practice is simple. Start with your monthly after-tax income, then split it into the three buckets. Adjust your spending so it fits, and let the percentages guide your decisions.

You do not need fancy tools. A simple note, three bank accounts, or a basic app is enough. The goal is to see roughly where your money is going and steer it toward the right buckets.

“You do not need complex software. You need three clear buckets and the will to fill them.”

How to start:

- Find your income — your monthly take-home pay.

- Split it — calculate 50%, 30%, and 20%.

- Adjust spending — shape your expenses to fit the buckets.

Adapt It to Your Reality

The 50/30/20 rule is a guideline, not a law. For many people, especially on lower incomes or in high-cost cities, needs may take more than 50%. That is okay, the rule is a starting point, you can adapt.

The real value is in the mindset: consciously dividing money between needs, wants, and the future. Tweak the percentages to fit your life, as long as you always save something and keep wants in check.

“The exact numbers matter less than the habit of giving every rupee a purpose.”

How to adapt it:

- Tweak the split — adjust percentages to your situation.

- Protect savings — always keep some going to the future.

- Aim to improve — move gradually toward the ideal balance.

The Takeaway

The 50/30/20 rule strips budgeting down to its simplest, most useful form. By dividing your income into needs, wants, and savings, you get a clear, flexible plan that covers your life today while building your future.

Here is the whole idea in one glance:

- 50% Needs — essentials you cannot skip

- 30% Wants — guilt-free spending on what you enjoy

- 20% Savings — wealth-building and extra debt payments

- Apply it — split your income into three buckets

- Adapt it — adjust the numbers to your reality

- The habit — give every rupee a clear purpose

“Budgeting is not about restriction. It is about telling your money where to go.”

Work out your three buckets this week using your last month’s income. Even a rough split will show you where your money is going and how to steer it better.

Have you tried the 50/30/20 rule? Share your experience in the comments, and pass this on to someone who wants to start budgeting simply.

Leave a Reply