Investing is not a “set it and forget it” activity. Many investors start their journey with great enthusiasm, picking the right stocks or mutual funds, but then they leave their portfolios untouched for years. While patience is a key, ignoring the balance of your investments can also lead to unwanted risks. This is where Portfolio Rebalancing comes in.

This article helps with step-by-step approach to rebalancing of your portfolio and reduce risk.

1. Why Portfolio Rebalancing Matters

Rebalancing is a vital exercise to ensure your portfolio does not become too risky or too conservative due to market movements. Since gold and equities often move in opposite directions, and bonds provide a safety net, maintaining your target ratio is the key to long-term wealth. If the stock market zooms up, your portfolio might become too heavy on equity, making you vulnerable to a sudden crash. Conversely, if markets fall, you might end up with too little equity, missing out on the recovery.

2. Set Allocation in Equity, Debt, and Gold Assets

Before you can fix your portfolio, you must have a “base” plan or define your assete allocation. A standard allocation might look like this but decide yourself how would you like to baseline this:

Equity (60%): This is for long-term growth and beating inflation. It includes Large-cap, Mid-cap, and Small-cap stocks or mutual funds.

Bonds/Debt (30%): This provides stability and regular income. This includes PPF, Fixed Deposits, and Debt Mutual Funds.

Gold (10%): This acts as a “shock absorber” against inflation and global crises.

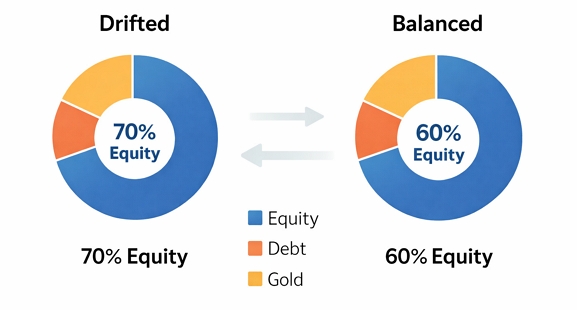

3. Check for Re-Balancing

Over time, different assets grow at different speeds. Calculate the current percentage of each asset in your total wealth. If your equity has performed exceptionally well, it might now make up 70% of your portfolio, while gold has shrunk to 5%. This change from your original plan is called “drift.”

When should you take action? You don’t need to check your portfolio every day. In fact, doing so might lead to emotional decisions. There are two professional ways to time your rebalancing:

Time-based: Review your portfolio every 6 or 12 months. Many investors prefer doing this at the start of the new financial year.

Threshold-based: Rebalance only if an asset moves by more than 5% from its target. For example, if your equity target is 60%, you only act if it hits 65% or drops to 55%.

4. Execution Strategies

There are two primary ways to bring your portfolio back to its original shape. Choosing the right one depends on how much money you have and your tax situation.

| Method | How it Works | Best For |

|---|---|---|

| The Buy/Sell Method | Sell a portion of the “winner” (e.g., Equity) and use that money to buy more of the “underperformer” (e.g., Gold). | Large portfolios or when the drift is significant and needs immediate fixing. |

| The New Inflow Method | Direct your new SIPs or lumpsum bonuses only into the underweight assets until the balance is restored. | Investors who want tax efficiency; it avoids selling and triggering capital gains. |

5. Common Mistakes to Avoid

Rebalancing in requires a bit of extra care due to taxes and rules. Here is what you need to keep in mind:

Tax Implications: Selling equity held for less than 12 months triggers Short-Term Capital Gains (STCG) at 15%. For debt and gold (including Sovereign Gold Bonds or Gold ETFs), be mindful of the latest 2025-26 tax slabs as indexation benefits have changed. Always calculate your tax before you sell.

Exit Loads: Most mutual funds charge an “exit load” (typically 1%) if you sell your units before a year. Ensure you are not losing money to these fees before you redeem your units for rebalancing.

Sovereign Gold Bonds (SGB): If you hold SGBs, rebalancing by selling might be difficult due to low liquidity on the secondary market (the stock exchange). In such cases, using the “new inflows” method to buy other assets is much more practical.

6. Rebalancing Checklist

To keep your wealth-building journey on track, follow this simple checklist:

1. List all current values from your investment apps.

2. Compare them against your original 60/30/10 target.

3. Decide whether to sell the “winners” or just redirect new SIP money.

4. Check for tax and exit load implications.

5. Confirm the final ratios align with your risk appetite.

Leave a Reply