Health insurance is one of the smartest financial decisions you can make. A single serious illness or hospital stay can wipe out years of savings, and good cover protects you from exactly that. There is no debate on this.

But here is the problem. When you go to buy it, you are often sold far more than you need. Agents push expensive add-ons, fancy riders, and inflated plans, playing on your fear of “what if.” You end up paying for cover you will likely never use.

The skill is knowing the difference between what health insurance you genuinely need to be protected and what is just an unnecessary, costly extra. Get this right, and you’ll stay well-protected without wasting money. Here is a clear guide.

“Good health insurance protects your savings. Bad health insurance drains them.”

Let us separate the essential from the unnecessary.

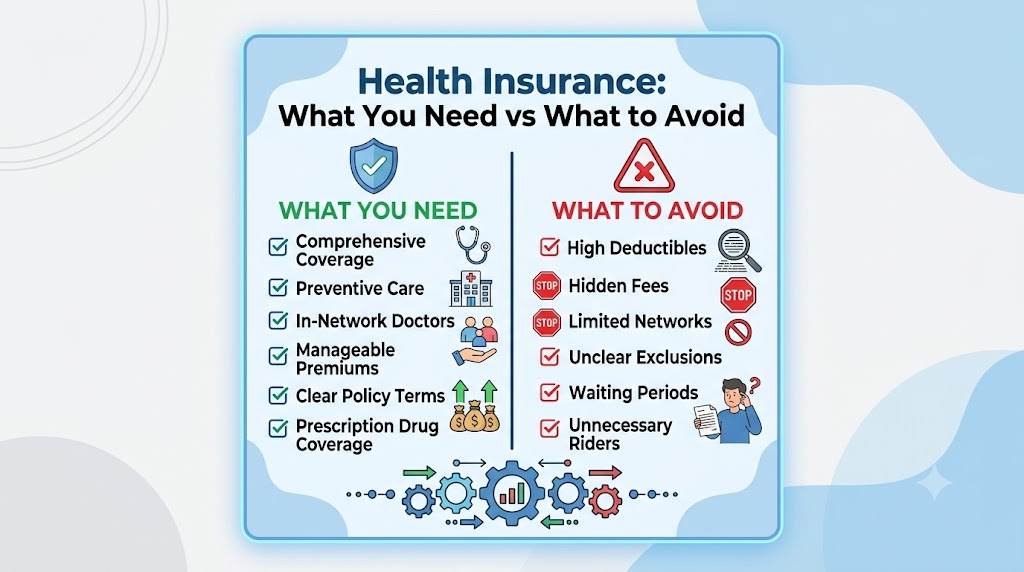

1. What You Genuinely Need

Let us start with the non-negotiables. There are a few things every person or family should have in their health cover. These form the foundation of real protection.

Skipping these, your insurance may fail you when you need it most. This is where your money is truly well spent. Basic genuine requirements are Adequate Cover to handle serious hospitalisation, a family floater (if you have a family at the moment), unlimited room rent (must have), pre- and post-hospitalisation cover, Day care treatment, no co-pay, a short waiting period, a good number of network hospitals for cashless treatment, and a nearby multi-speciality hospital.

“Cover the big risks well before you worry about the small extras.”

The essentials to have:

- Adequate cover amount — enough to handle a serious hospitalisation, not a token sum.

- A family floater (if you have a family) — one plan covering the whole family, often cost-effective.

- Cashless hospital network — so you are not scrambling for funds during a crisis.

2. Get Enough Cover, Not Too Little

The most common and dangerous mistake is buying a plan with too small a cover amount, just to save on the premium. Medical costs have risen sharply, and a small cover can run out fast during a major illness.

It is far better to have adequate cover for serious situations than a cheap plan that barely helps. Think about the cost of a real hospitalisation today, not what felt like a lot years ago.

“A cover too small to help in a crisis is money half-wasted.”

How to size your cover:

- Think big-illness — cover should handle a serious, costly hospitalisation.

- Account for rising costs — medical inflation makes old amounts inadequate.

- Review it periodically — raise your cover as costs and needs grow.

3. Consider Cover Beyond Employer Insurance

Many people rely only on the health insurance provided by their employer and assume they are fully covered. This is a risky gap. Employer cover ends the moment you leave or lose the job.

Having your own personal health policy, separate from your employer’s, means you stay protected regardless of your job situation. This is one piece of “extra” cover that is genuinely worth having.

“Employer insurance lasts as long as the job. Your own cover lasts as long as you need it.”

Why personal cover matters:

- Job-independent — stays with you through job changes.

- Continuous protection — no dangerous gaps between jobs.

- Builds over time — early, continuous cover pays off later.

4. Useful Add-Ons Worth Considering

Not all add-ons are a waste. A few riders can genuinely strengthen your protection at a reasonable cost and are worth considering depending on your situation. The key is to choose based on real need.

These are worth a look, but only if they fit your circumstances, not just because an agent recommends them. Evaluate each one to see whether it addresses a real risk for you.

“A good add-on solves a real problem. A bad one just adds to the premium.”

Add-ons that can be worthwhile:

- Restoration benefit — refills your cover if it runs out in a policy year.

- No-claim bonus — increases your cover for claim-free years.

- Critical illness cover — a lump sum for major illnesses, if relevant to you.

5. What Is Often Unnecessary

Now the other side. Many extras are pushed hard but add little real value for most people. They inflate your premium while covering risks that are unlikely or minor. Be wary of these.

You do not need every rider under the sun. Focus your money on solid core coverage, and be sceptical of expensive extras that sound impressive but rarely pay off.

“The fanciest plan is not the best plan. It is often just the most expensive one.”

Commonly oversold extras:

- Too many niche riders — narrow add-ons for unlikely situations.

- Overlapping cover — paying twice for what you already have.

- Gimmicky perks — flashy features that rarely get used.

6. Read the Fine Print

Whatever you buy, the details matter enormously. Two plans with the same cover amount can be very different once you look at exclusions, waiting periods, and claim conditions. This is where many people get caught out.

Before buying, understand what is and is not covered, the waiting periods, and how claims work. A slightly cheaper plan with poor terms can cost you dearly when you actually need it.

“The cheapest plan can be the costliest one when you read the fine print.”

What to check carefully:

- Exclusions — what the plan does not cover.

- Waiting periods — delays before certain conditions are covered.

- Claim process — how easy or hard it is to actually claim.

The Takeaway

Health insurance is essential, but more is not always better. The goal is smart cover, strong protection where it matters, without wasting money on unnecessary extras pushed by eager sellers.

Here is the whole plan at a glance:

- Get enough cover — adequate for a serious illness

- Buy your own — do not rely only on employer insurance

- Choose add-ons wisely — only those that solve real risks

- Skip the gimmicks — avoid oversold, unlikely-to-use extras

- Read the fine print — exclusions and claim terms matter most

“Insure well against the big risks, and stop paying for the ones that barely matter.”

Review your health cover this week, or if you have none, start looking into a solid plan. Focus on strong core protection, and do not let anyone upsell you into waste.

How do you decide what health cover you need? Share your thoughts in the comments, and pass this on to someone shopping for insurance.

Leave a Reply